The answer to your question is negative: such a function $f$ does not exist.

Indeed, given the distribution functions (d.f.'s) $F$ and $G$ of random variables (r.v.'s) $X$ and $Y$, the smallest value of $E|X-Y|$ is the Wasserstein distance between their distributions, which equals

$$d(F,G):=\int_0^1|F^{-1}(u)-G^{-1}(u)|\,du;

$$

see e.g. (2) in [1], where

$$F^{-1}(u):=\inf\{x\in\mathbb R\colon F(x)\ge u\}.

$$

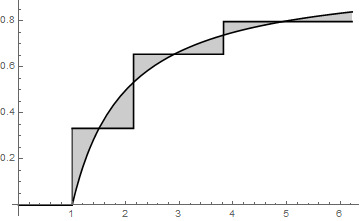

Let $F(x)=(1-1/x)I\{x>1\}$ for real $x$, where $I\{\cdot\}$ is the indicator function. Then $F$ is the distribution function (d.f.) of a random variable (r.v.) $X$.

Take any real $\epsilon>0$ and let $h_n:=\epsilon/\sqrt n$ for natural $n$.

Define $x_n\ge1$ and $y_n>x_n$ for natural $n$ by induction. Let $x_1:=1$. For all natural $n$, let $y_n:=(1+h_n)x_n$. For $z\ge x_n$, let

$$d_n(z):=\int_{x_n}^z\Big(\frac1x-\frac1{y_n}\Big)\,dx=\ln\frac z{x_n}-\frac{z-x_n}{y_n}.

$$

Then $d_n$ continuously decreases on $[y_n,\infty)$ from $d_n(y_n)>0$ to $-\infty$. So, for some unique $x_{n+1}>y_n$ one has

$$0=d_n(x_{n+1})=\int_{x_n}^{x_{n+1}}\Big(\frac1x-\frac1{y_n}\Big)\,dx.

$$

Thus, $x_n$ and $y_n$ are defined for all natural $n$, with $x_n<y_n<x_{n+1}$.

Define now the d.f. $G$ of a r.v. $Y$ by the conditions: $G=F[=0]$ on $(-\infty,1)$ and $G=F(y_n)=1-1/y_n$ on $[x_n,x_{n+1})$ for each natural $n$. Then

$$\int_{\mathbb R}|F(x)-G(x)|\,dx\ge\sum_{n=1}^\infty\int_{x_n}^{y_n}|F(x)-G(x)|\,dx

=\sum_{n=1}^\infty d_n(y_n)=\infty,

$$

since $d_n(y_n)=\ln(1+h_n)-\frac{h_n}{1+h_n}\sim h_n^2/2=\epsilon^2/(2n)$.

On the other hand, for any real $t>1$, let $n=n_t$ be the unique natural number such that $x_n<t\le x_{n+1}$; then

$$|E(t-X)_+-E(t-Y)_+|

=\Big|\int_{-\infty}^t(F(x)-G(x))\,dx\Big|$$

$$=d_n(t)\le d_n(y_n)<\epsilon^2/(2n)\le\epsilon^2/2,

$$

and $|E(t-X)_+-E(t-Y)_+|=0$ if $t\le1$. (I use $-X,-Y,t=-K$ instead of your $X,Y,K$.)

Thus, $\sup_{t\in\mathbb R}|E(t-X)_+-E(t-Y)_+|\le\epsilon^2/2$, which can be made arbitrarily small, while

the smallest value of $E|X-Y|$ for r.v.'s $X$ and $Y$ with these d.f.'s $F$ and $G$ is

$d(F,G)=\int_0^1|F^{-1}(u)-G^{-1}(u)|\,du=\int_{\mathbb R}|F(x)-G(x)|\,dx=\infty$; the penultimate equality here reflects the two ways to compute the area between the graphs of $F$ and $G$ (which is the same as the area between the graphs of $F^{-1}$ and $G^{-1}$).

Here the graphs of these $F$ and $G$ are shown for $\epsilon=0.5$; each even-numbered gray area equals the preceding odd-numbered gray area:

Remark. Instead of $h_n:=\epsilon/\sqrt n$, one could simply set $h_n:=h:=\epsilon$, so that $h_n$ not depend on $n$. Then the proof would be simplified a bit. However, with $h_n:=\epsilon/\sqrt n$, one has the extra property that $E(t-X)_+-E(t-Y)_+\to0$ as $t\to\infty$.