Here is a simple counterexample that is a bit too long for a comment.

Consider two discrete-time Markov chains on $S=\{1,2,3\}$ with the following two transition matrices: $$ P_1 = \begin{bmatrix} 0 & 1 & 0 \\ 0 & 0 & 1 \\ 1 & 0 & 0 \end{bmatrix} \;, \quad P_2 = \begin{bmatrix} 0 & 1/2 & 1/2 \\ 1/2 & 0 & 1/2 \\ 1/2 & 1/2 & 0 \end{bmatrix} $$ Both chains are irreducible and leave the uniform distribution invariant. The corresponding discrete-time Markov chains have the same lag-$1$ equilibrium autocorrelation, i.e., $\ell_1=-1/2$. However, for $k>1$ their lag-$k$ autocorrelations are quite different since the first chain is periodic with period $3$ while the second chain's lag-$k$ autocorrelation decays to zero with $k$.

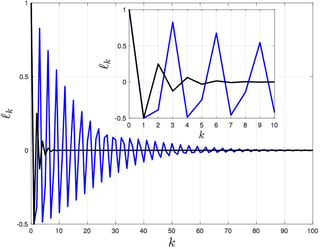

This is not quite a counterexample, since the first chain does not have a steady-state or limiting distribution. To correct this deficiency, we break its periodicity by slightly perturbing its entries using a small parameter $\epsilon>0$: $$ \tilde P_1 = \begin{bmatrix} 0 & 1-\epsilon & \epsilon \\ \epsilon & 0 & 1-\epsilon \\ 1-\epsilon & \epsilon & 0 \end{bmatrix} $$ The lag-$k$ correlation functions for the chains with transition matrices $\tilde P_1$ (blue line) and $P_2$ (black line) are plotted below with $\epsilon=1/25$ (chosen for visualization purposes only). The inset shows the first few lag correlations. Note that $\ell_1$ is the same for the two chains.

ADD

As the OP (HolyMonk) points out in the comments to this answer: for $\tilde P_1$ (given above) and for any $\epsilon>0$, we have $\ell_1 = -1/2$ and $\ell_2 = -1/2−3(−1+ϵ)ϵ$.