Consider the stochastic process

$$f(B_t)$$

where $B_t$ is standard Brownian motion (or the Wiener process) and $f$ is a twice-differentiable function.

Ito’s lemma states that

$$df = f'(B_t) dB_t + \frac{1}{2} f''(B_t) dt$$

The first term is recognizable from the chain rule in classical calculus, but why the second term? If $dB_t$ is truly infinitesimal, it doesn’t even seem possible that $df \neq f'(B_t) dB_t$.

To understand Ito’s lemma intuitively, think of $dB_t$ as a little stochastic variable, specifying $B_t$‘s change during the next $dt$.

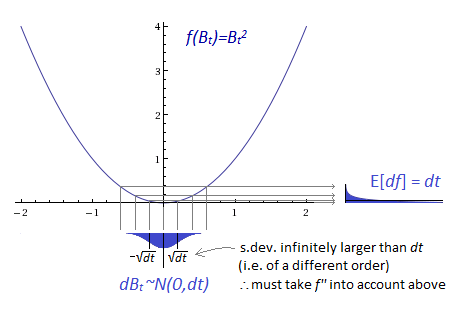

$$dB_t = B_t - B_{t+dt} \sim N(0,dt)$$

This models Brownian motion (or the Wiener process) completely. Now $df$ should be a little stochastic variable too, modeling the stochastic process $f(B_t)$.

The picture at the start considers an example $f(B_t)$ where $f'(B_t)=0$, thereby suppressing the “intuitive” or classical term in Ito’s lemma. The reason why $df>0$ in that picture is the reason why that “non-intuitive” term is needed.

Loosely speaking, wherever $f$ has curvature, $dB_t$ will diffuse around that curvature sufficiently to influence the expected result on the order of $dt$. (The specific example in the picture makes this trivial, as $f(\sqrt{t}) = t$.)

Why doesn’t $dB_t$ dominate away $(dB_t)^2$ (i.e. $dt$ )? Because $E[(dB_t)^2]$ does not come from $(E[dB_t])^2$ as happens with classical differentials. The strong law of large numbers implies that a stochastic differential’s expected value pushes its integral on a faster order than its deviation does.