I solved the problem by reformulating it using an economic argument.

I find it astonishing how simple the problem becomes after the reformulation/reconceptualization.

I believe there must be a form of mathematical mapping that projects the original problem onto the new problem and I am very curious what that could be.

The argument I use is economic in nature and is probably quite "chatty" for a mathematician.

The Economic Problem

As it is key to my argument, I write the economic problem once again, adding some important details.

The buyer

One buyer wants to buy maximally $J$ units.

For each unit he buys, he earns $v$.

The number of units that is offered to him is $j$.

Thus, for example, with $v=10$ and $j=3, 4, 5, 6, \text{and } 7$, the buyer earns $30, 40, 50, 50, \text{and } 50$.

The price per unit depends on the supply, but has a maximum, $CAP$, set by the buyer.

The number of units that is offered, $j$, follows a random distribution.

When the number of units $j \leq J$, the supply is less than demand, and the price per unit is as high as possible, $CAP$

When the number of units $j > J$, the price per unit is $- \delta C$, where $C$ is the fixed cost of a unit.

The sellers

There are $J$ identical sellers.

Each sellers has a fixed cost of $C$.

For a seller to become eligible to sell to the buyer,

it has to enter the market and I assume that this involves making a sunk investment equal to a proportion of it's cost, $\delta C$.

All sellers decides simultaneously to become eligible with probability $q$.

The probability $q$ is determined so that the sellers make zero profits in expectation.

Variables

Then:

- $0<q<1$ is the probability of a a unit being offered

- $v>0$ is the value of a unit for the buyer \

- $C>0$ is the fixed cost of the unit for the seller and $C<<v$ \

- $0<- \delta C<C$ is the \textit{negative} price of a unit when $j>J$.\

- $CAP>C$ is the price of a unit when $j \leq $ and a parameter to set by the buyer.

The Original Formulation

The buyer wants to maximize its profit leads and thus originally I started out writing the Lagrangian:

\begin{align*}

\mathcal{L}[CAP,q,\lambda]

=&

(v-CAP) \sum_{j=1}^J j \cdot q^j (1-q)^{N-j} \binom{N}{j} \\

& +

(v- c + \delta C) \sum_{j=J+1}^{N} J \cdot q^j (1-q)^{N-j} \binom{N}{j} \notag \\

& +

\lambda \Bigg\{(CAP-C) \sum_{j=1}^J q^{j-1} (1-q)^{N-1-j} \binom{N-1}{j-1} \notag \\

& -

\delta C \sum_{j=J+1}^{N} q^{j-1} (1-q)^{N-1-j} \binom{N-1}{j-1} \Bigg\} \notag &&

\end{align*}

However, as detailed in my post above, this approach led to a non-concave objective function and the proof that the Lagrangian has slope zero when $CAP=v$ alone is torturous,

Moreover, the proof does not establish it is a maximum, let alone a global maximum.

Alternative (but equivalent) Formulation

The problem can be reformulated after applying some economic intuition.

The question I ask is in what precise cases the buyer's profit decreases.

There are two such cases.

1. Over-entry

When $j>J$ sellers decide to enter, then $j-J$ of them will not be able to sell and have made the sunk cost, $\delta C$, in vain.

I call this a case of "over-entry": Too many sellers entered the market.

The expected loss due to over-entry is thus $( \delta C ) \sum_{j=J+1}^N (j-J) \cdot q^{j} (1-q)^{N-j} \binom{N}{j}$.

As the sellers make zero profit by assumption, this loss is paid by the buyer and thus decreases the buyer's profit.

2. Under-entry

When $j<J$ sellers decide to enter, then the buyer loses out on the opportunity to buy $J-j$ items.

I call this a case of "under-entry": Too few sellers entered the market.

Each of those lost sales would have increased his profit by $(v-C)$, the value the buyer has for the item minus the cost of producing that item.

The expected loss due to under-entry is thus $( v- C ) \sum_{j=0}^J (J-j) \cdot q^{j} (1-q)^{N-j} \binom{N}{j}$.

Thus the buyer basically would like to minimize these two factors that decrease his profits.

Let's call this the loss function.

Then:

\begin{align*}

loss[q]=&( \delta C ) \sum_{j=J+1}^N (j-J) \cdot q^{j} (1-q)^{N-j} \binom{N}{j} \\

&+

( v- C ) \sum_{j=0}^J (J-j) \cdot q^{j} (1-q)^{N-j} \binom{N}{j}

\end{align*}

With, as in the original problem, the restriction:

\begin{align*}

&(CAP-C) \sum_{j=1}^J q^{j-1} (1-q)^{N-1-j} \binom{N-1}{j-1} \notag

=

\delta C \sum_{j=J+1}^{N} q^{j-1} (1-q)^{N-1-j} \binom{N-1}{j-1}

\end{align*}

The only free parameter for the buyer is to set $CAP$.

Setting $CAP$ affects the probability of entry through the restriction $q$.

I can thus solve the problem by finding the $q$ that minimizes $loss[q]$ and use the restriction then to determine the corresponding $CAP$.

Solving the Alternative Formulation

Let us thus differentiate $loss[q]$ and set it equal to zero.

\begin{align*}

0=&\frac{d loss[q]}{d q} \\

=& \delta C \sum_{j=J+1}^N (j-J) \Big(j \cdot q^{j-1} (1-q)^{N-j} \\

&-(N-j) \cdot q^{j} (1-q)^{N-1-j} \Big) \cdot \binom{N}{j} \\

&+

( v- C ) \sum_{j=0}^J (J-j) \Big(j \cdot q^{j-1} (1-q)^{N-j} -(N-j) \cdot q^{j} (1-q)^{N-1-j} \Big) \cdot \binom{N}{j} \\

=& \delta C \Bigg(

\sum_{j=J+1}^N (j-J) j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j} \\

&-

\sum_{j=J+1}^N (j-J) (N-j) \cdot q^{j} (1-q)^{N-1-j} \binom{N}{j}

\Bigg) \\

&+

( v- C ) \Bigg( \sum_{j=0}^J (J-j) j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j} \\

&-

\sum_{j=0}^J (J-j) (N-j) \cdot q^{j} (1-q)^{N-1-j} \binom{N}{j}

\Bigg) \\

=& \delta C \Bigg(

\sum_{j=J+1}^N (j-J) j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j} \\

&-

\sum_{j=J+2}^{N+1} (j-1-J) (N+1-j) \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j-1}

\Bigg) \\

&+

( v- C ) \Bigg( \sum_{j=0}^J (J-j) j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j} \\

&-

\sum_{j=1}^{J+1} (J+1-j) (N+1-j) \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j-1}

\Bigg) \\

=& \delta C \Bigg(

\sum_{j=J+1}^N (j-J) j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j} \\

&-

\sum_{j=J+1}^N (j-1-J) j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j}

\Bigg) \\

&+

( v- C ) \Bigg( \sum_{j=0}^J (J-j) j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j} \\

&-

\sum_{j=0}^J (J+1-j) j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j}

\Bigg) \\

=& \delta C \Bigg(

\sum_{j=J+1}^N j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j}

\Bigg) \\

&-

( v- C ) \Bigg(

\sum_{j=0}^J j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j} + J \cdot q^{J-1} (1-q)^{N-J} \binom{N}{J}

\Bigg)

\end{align*}

Using the restriction to substitute for the term $\delta C \Bigg(

\sum_{j=J+1}^N j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j}

\Bigg) $ gives:

\begin{align*}

0=& (CAP-C) \Bigg(

\sum_{j=0}^J j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j}

\Bigg)

-

( v- C ) \Bigg(

\sum_{j=0}^J j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j}

\Bigg) \\

=& (CAP-v) \Bigg(

\sum_{j=0}^J j \cdot q^{j-1} (1-q)^{N-j} \binom{N}{j}

\Bigg)

\end{align*}

We can thus conclude that $CAP \gtreqqless v \implies \frac{d loss[q]}{d q} \gtreqqless 0$ and $loss[q]$ is thus strictly convex and therefore has a global minimum at $CAP=v$.

Of course, given the setup, this implies that the buyer's profit reaches a global maximum at $CAP=v$.

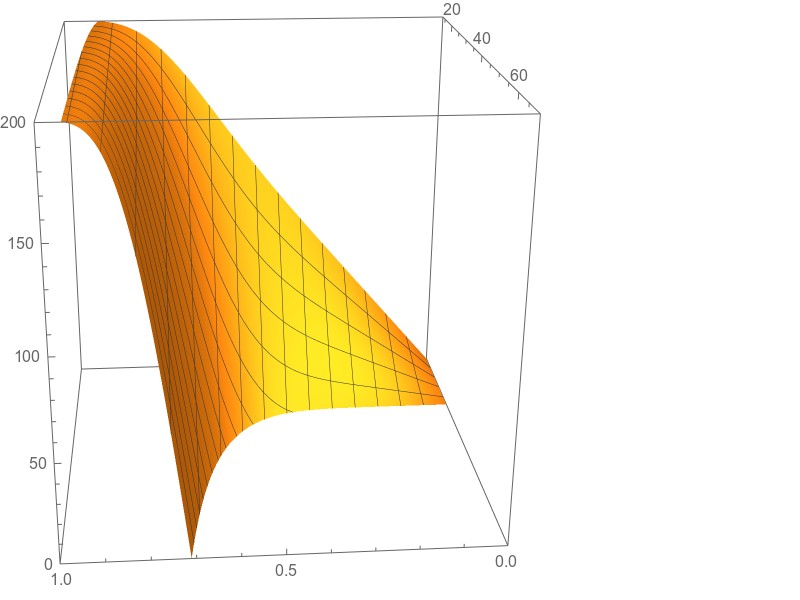

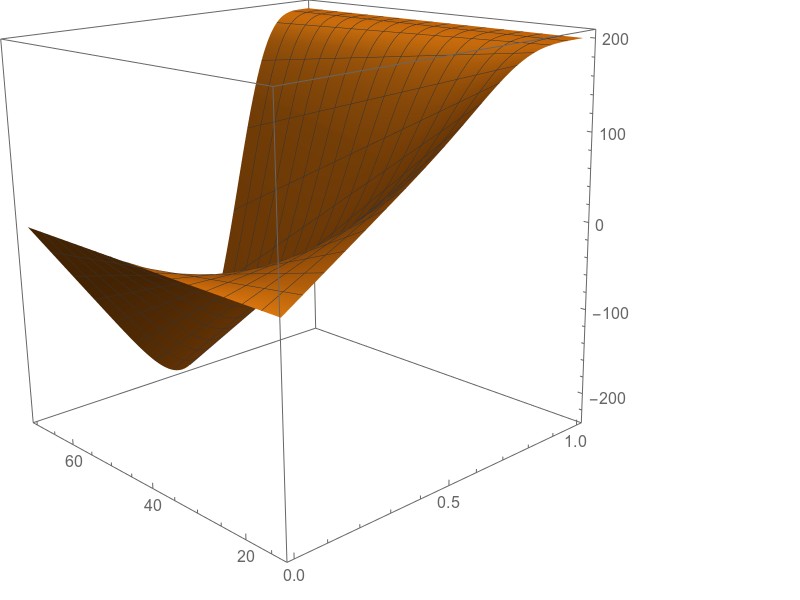

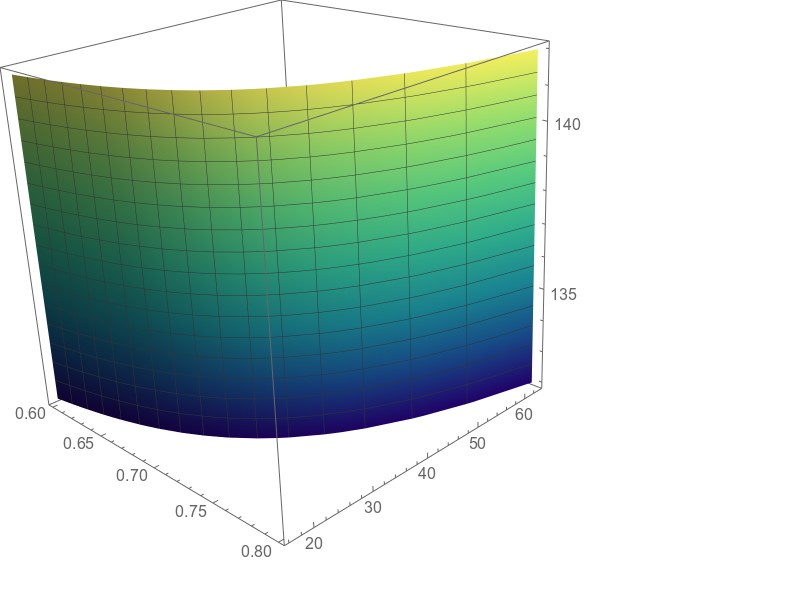

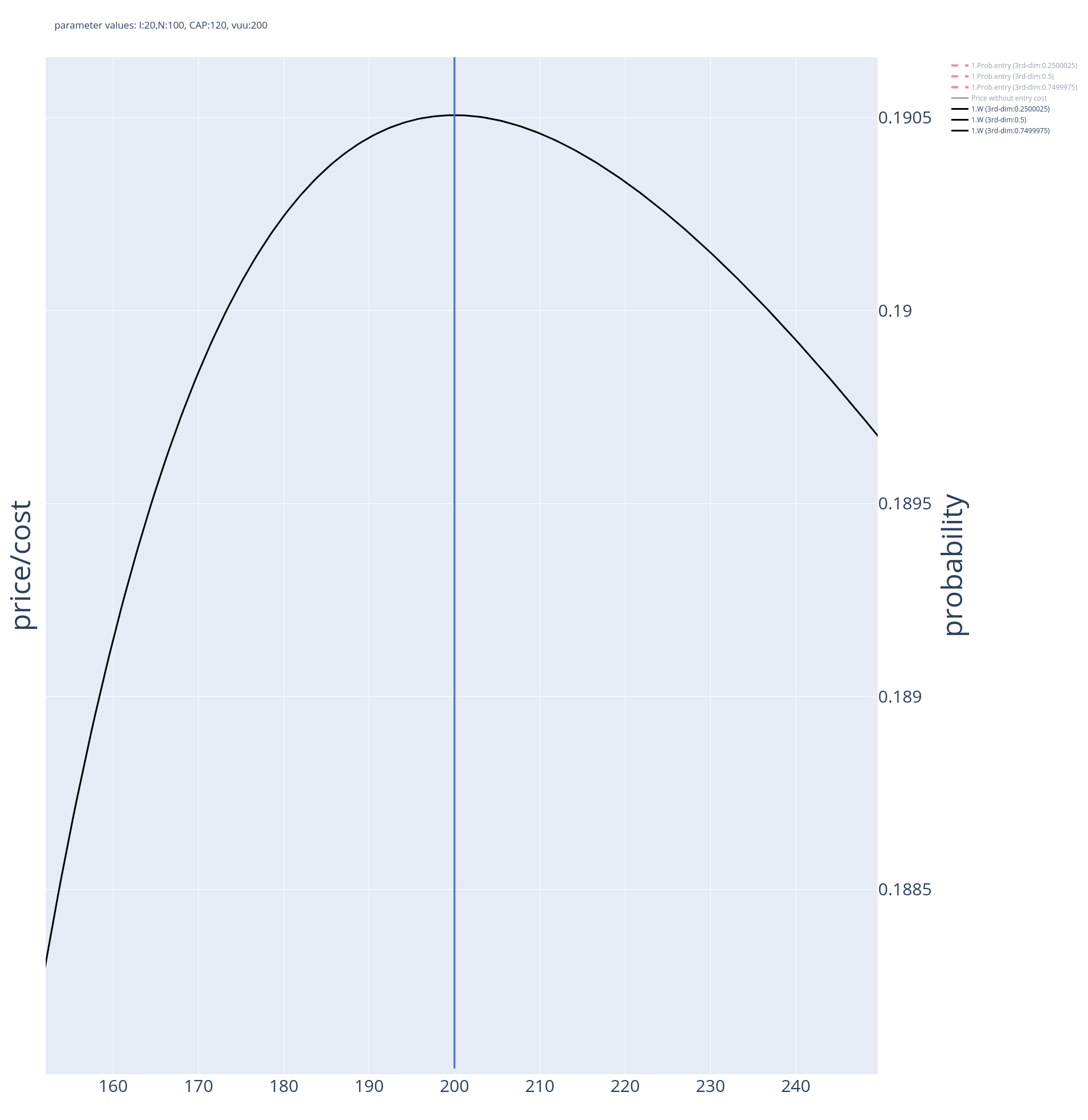

Fig.2:Objective Function - different angle

Fig.2:Objective Function - different angle

The vertical line indicates the maximum. In the graph $v=200$. The plot in Fig.5 clearly shows how the maximum is attained at $CAP=200=v$ and that this is a global optimum (for the specific parameter values used to draw Fig.5).

The vertical line indicates the maximum. In the graph $v=200$. The plot in Fig.5 clearly shows how the maximum is attained at $CAP=200=v$ and that this is a global optimum (for the specific parameter values used to draw Fig.5).