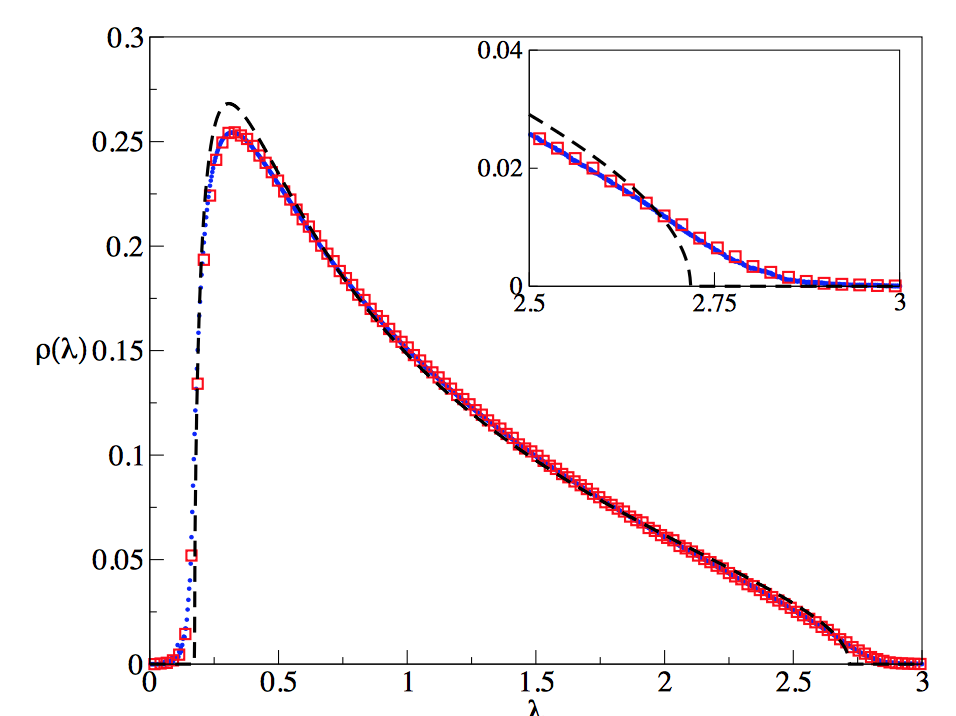

I was wondering if anyone knew of any results regarding the limiting distribution of singular values for sparse random real-valued matrices?

Specifically, let $X$ be an $N\times M$ matrix with real-valued entries, with $X_{ij} = a_{ij}K_{ij}$, where the nonzero entries $K_{ij}\sim N(0, \sigma^2)$ i.i.d, and $a_{ij} = 1$ with probability $p$ and $0$ with probability $1-p$, i.i.d. We can assume here that $p = O(N^{-d})$ where $d > 0$.

What is known about analytically about the limiting distribution of the distribution of singular values of $X$ (or equivalently, the eigenvalue distribution of $X^TX$)?

There is a lot of literature on random matrix theory, and I figured there must be a result about this somewhere as this would be a variant of the Marchenko-Pastur law where the matrix has a well-defined sparsity. Pointers to references would be good too!