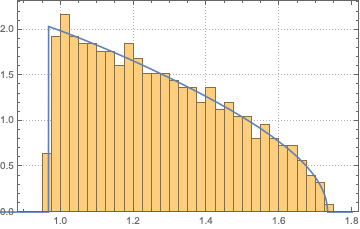

Let $\lfloor{*}\rfloor$ denotes the nearest integer $\le *$. I'm asking myself the question what's the limit of the part of the empirical spectral distribution corresponding to the first $\lfloor{p/2}\rfloor$ eigenvalues of the sample covariance matrix?

To be more precise, assume that $X=[x_1,...x_n]=[x_{ij}]_{1\le i,j \le n}$ is a $p\times n$ random matrix, where $x_i$'s are individual iid random sample, so that the entries of $X$, namely $x_{ij}$, are iid random variable with mean $0$, variance $1$ and bounded fourth moments.

Next consider: the random measure $Head_{n,p}:=\frac{1}{\lfloor{p/2}\rfloor}\sum_{i=1}^{\lfloor{p/2}\rfloor}\delta_{\lambda_i}$, where $\lambda_1 \ge \lambda_2 \ge \lambda_{\lfloor{p/2}\rfloor}\ge \ldots \ge \lambda_p$ are the eigenvalues of $\frac{1}{p}XX^{T}$.

Then the question is: what's the limit

$$\lim_{n,p \to \infty, p/n \to c \in (0, \infty)} Head_{n,p}?$$

Intuitively, I'd first guess that it should be the Marcenko Pastur distribution with the $c$ replaced by $c/2$, as $\frac{\lfloor{p/2}\rfloor}{n}\to \frac{c}{2}$ as $\frac{p}{n}\to c$, and that one can construct a random matrix $Y \in \mathbb{R}^{ \lfloor{p/2}\rfloor\times n}$ so that all the $\lfloor{p/2}\rfloor$ eigenvalues of $YY^{T}$ correspond to the first $\lfloor{p/2}\rfloor$ eigenvalues of $X$. But then the question would be what can we say about the limit of the following random measure that's a sum of Dirac measures the last $\lfloor{p/2}\rfloor$ eigenvalues? Mathematically that is: what's the limit of

$$Tail_{n,p}:=\frac{1}{\lfloor{p/2}\rfloor}\sum_{i=\lfloor{p/2}\rfloor}^{p}\delta_{\lambda_i}?$$

If I were correct, this should also be the Marcenko Pastur distribution with the $c$ replaced by $c/2$, but I feel it isn't.

Somewhat more generally, one can assume that $p\to \infty$ being a multiple of $q$, i.e. being of the form $p=kq, k\to \infty$ Let $ r, s \in \mathbb{N}$ fixed, and then we can ask for the limit of the random measure:

$$lim_{p,n \to \infty , \frac{p}{n} \to c \in (0,\infty)}\frac{1}{sq-rq}\sum_{i=rq+1}^{sq}\delta_{\lambda_i}$$