I'm teaching a financial mathematics course and have found a fascinating (to me) numerical phenomenon and wonder if anyone has studied it, or knows anything similar.

I'll try and give a description of what it means followed by a self-contained description of what I'm doing. First of all: an American put option is a product that gives the right to sell a share for a price $K$ (agreed at the outset) at any time up to the expiry time, $t$, of the option. It's assumed that the underlying share is moving according to a geometric Brownian motion (GBM) with known volatility parameter $\sigma$. The interest rate is $r$ and the initial share price is $s$.

The basic idea is to discretize the GBM to a multiplicative random walk on the "binomial tree" with depth $n$. That is: one assumes that at each of the $n$ stages the price multiplies by $u=\exp(\sigma\sqrt{t/n})$ or $d=1/u$. In this derivation, the "risk-neutral measure" is the measure on the multiplicative random walk where up steps occur independently with probability $p=(\exp(rt/n)-d)/(u-d)$ and down steps occur with probability $q=1-p$. One can then define $V_{j,i}$ to be the value of the option if unexercised by time $jt/n$ and the current share price is $su^id^{j-i}$. The approximate arbitrage-free cost of the option is $V_{0,0}$. The scaling of the multipliers guarantees that the multiplicative random walk converges to a geometric Brownian motion in the appropriate sense. It is assumed (and probably proved somewhere) that this converges to the true arbitrage free cost (computed using the GBM rather than the discrete approximation) as $n\to\infty$. I am interested in the dependence of $V_{0,0}$ on $n$, the number of time steps.

Here is the actual calculation that I'm doing: define $V_{n,i}=(K-su^id^{n-i})^+$. One then does a backwards recursion to populate previous levels of the "tree": $V_{j,i}=\max\big(K-su^id^{j-i},e^{-rt/n}(pV_{j+1,i+1}+qV_{j+1,i})\big)$. [The max here corresponds to either exercising the option now or holding it].

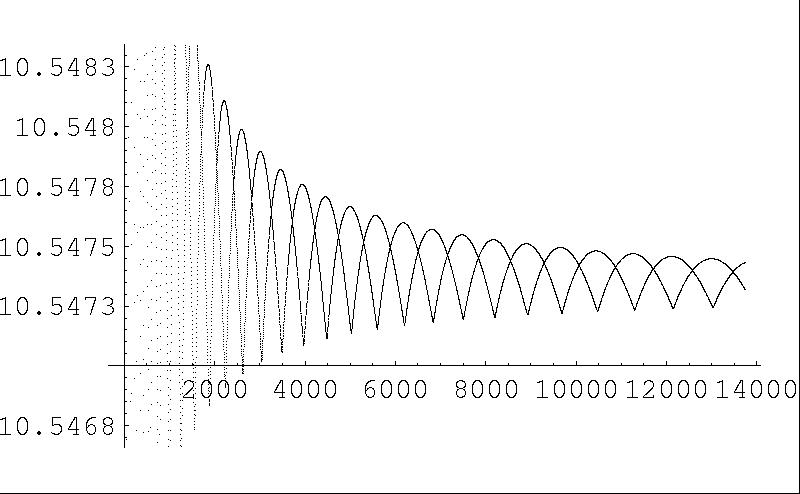

Here is a graph of $V_{0,0}$ versus $n$:

It seems that for odd $n$, the function roughly follows one curve, while for even $n$ it roughly follows another. I have no idea why the graph should look like this...