The techniques are similar to the answer here Small noise limits with irregular drift.

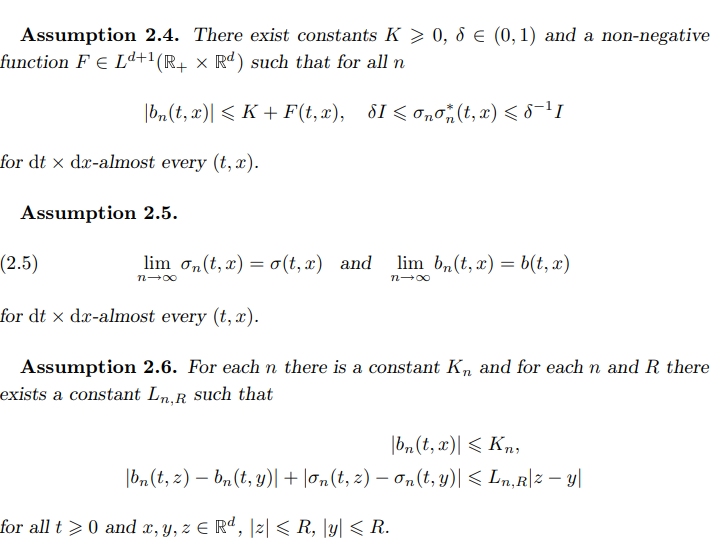

In the article "On stochastic differential equations with locally unbounded drift" they obtain a beautiful pointwise almost everywhere result for the coefficients that then gives uniform. So on that random set you have, we only need that eventually it converges to $\sigma$ almost everywhere.

The only caveat is that you need to assume uniform ellipticity for the volatility coefficient.

Then they get nice uniform convergence results.