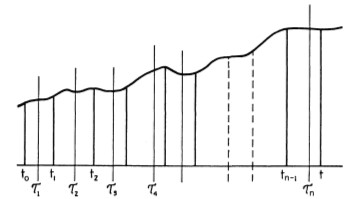

When we integrate a function, we must make some choice about how we approximate it before we take the limit.

In principle, we can choose $\tau_i$ to be any value between $t_{i-1}$ and $t_i$. But for an ordinary Riemann integral our choice doesn't matter since for any value of the intermediate point $\tau \equiv \frac{\tau_i}{t_i-t_{i-1}}$, we find the same value in the limit of vanishing box sizes.

For stochastic integrals, however, this is no longer the case. For example, for the Itô integral, we choose $\tau =0$, while for the Stratonovich integral we choose $\tau = 0.5$.

I'm wondering what feature of stochastic integrals leads to their dependence on the choice of $\tau$? (Since I'm a physicist by trade, a somewhat intutive argument would be great.)I'm wondering what feature of stochastic integrals leads to their dependence on the choice of $\tau$? (Since I'm a physicist by trade, a somewhat intutive argument would be great.)