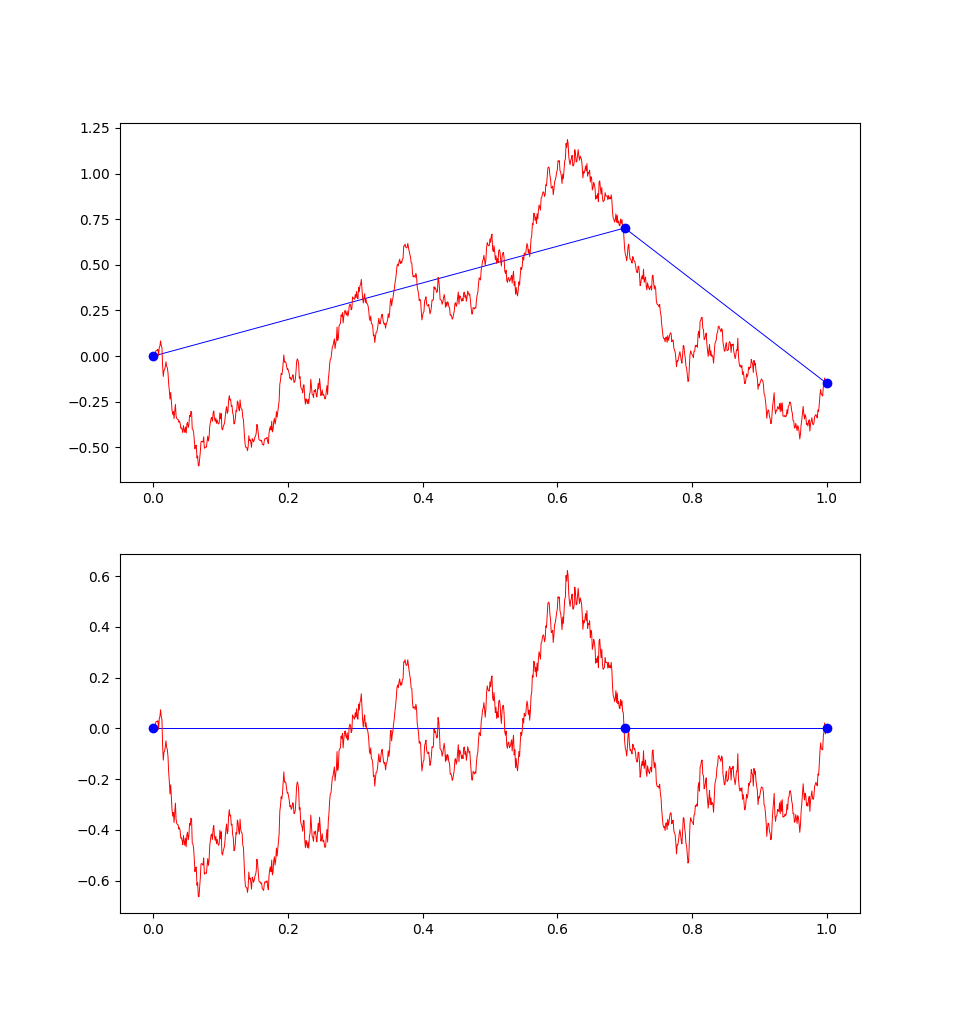

(I'm changing your notations a bit, because I want to call $B$ a Brownian bridge.)

Fix $0<s\leq1$, and let $W$ be a standard Brownian motion indexed by $[0,1]$. I call the (law of the) random variable $u\in[0,s]\mapsto B_u-\frac usB_s$$u\in[0,s]\mapsto W_u-\frac usW_s$ a Brownian bridge of size $s$. It is but the Brownian motion modified to be $0$ at $s$, by subtracting a linear function.

I claim that the "superposition" of a Brownian bridge $B$ of size $s$ and a normal variable $N$ of variance $1$ is a Brownian motion on $[0,1]$: here, superposition means the process $$u\mapsto B_u+uN\text.$$ One can prove this fact by noting that such a process is Gaussian, and has the desired finite dimensional covariances.

Now for what you're asking: the Brownian motion $W$ can be decomposed in for independent variables (see image below):

- two bridges $B$ and $B'$ of sizes $s$ and $1-s$;

- two Gaussian variables $N$ and $N'$ of variances $s$ and $1-s$.

(To prove this, I would go the other way around and show that given such random independent variables, the "superposition" is Gaussian and has the required covariance.)

Once this is done, we see that $$\mathcal{G}_t = \sigma(N,N',B)$$ and so $$ \mathbb{E}[W_t-W_s|\mathcal{G}_s] = \mathbb{E}\left[B'_{t_s} + \frac{t-s}{1-s}N'\middle|\mathcal{G}_s\right] = \frac{t-s}{1-s}N' = \frac{t-s}{1-s}(B_{1-s}-B_s)\text. $$