Let $b:=\beta$. Assume, more generally, that $-1<b<1$. To reflect the dependence on $b$, write $W_{i,b}$ and $Y_b:= \frac{1}{n}\sum_{i=1}^nW_{i,b}-b$ in place of $W_i$ and $Y$. The problem is equivalent to finding a bound on $P(X_b>x)$ for $X_b:=Y_b+b=\frac{1}{n}\sum_{i=1}^nW_{i,b}$, $x:=y+b$, $y>0$, and all $b\in(-1,1)$, because the left tail of $X_b$ is the same as the right tail of $X_{-b}$. That is, for all $y>0$ one has $P(Y_{|b|}>y)=P(X_b>y+b)$ if $b\in[0,1)$ and $P(Y_{|b|}<-y)=P(X_b>y+b)$ if $b\in(-1,0]$.

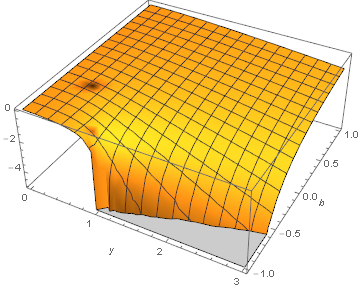

One can use an exponential bound. Note that, for independent standard normal random variables $Z_1$ and $Z_2$, the random set $\{U,V\}$ is equal in distribution to the random set $\{(Z_1-aZ_2)k,(Z_1+aZ_2)k\}$ if $k^2=\frac{1+b}2$ and $a^2=\frac{1-b}{1+b}$, whence $W=UV$ is equal in distribution to $(Z_1-aZ_2)(Z_1+aZ_2)k^2=k^2Z_1^2-k^2a^2Z_2^2=\frac{1+b}2\,Z_1^2-\frac{1-b}2\,Z_2^2$. So, for $0\le h<h_b:=\frac1{1+b}$, \begin{equation} E e^{hUV}=E e^{hk^2Z_1^2}E e^{-hk^2a^2Z_2^2}=\frac1{\sqrt{1-(1+b)h}}\,\frac1{\sqrt{1+(1-b)h}}, \end{equation} whence \begin{equation} P(X>x)\le E e^{nh(X-x)}=\exp\{n\ell(h)\}, \end{equation} where $$\ell(h):=\ell_{b,x}(h):=-hx-\tfrac12\,\ln\big(1-2bh-(1-b^2)h^2\big).$$ It is not hard to see that $\ell(h)$ is minimized at $h=h_{b,x}$, where \begin{equation} h_{b,x}:=\frac{\sqrt{\left(1-b^2\right)^2+4 x^2}-(1-b^2+2 b x)}{2 \left(1-b^2\right) x} \end{equation}\begin{equation} h_{b,x}:=\frac{\sqrt{\left(1-b^2\right)^2+4 x^2}-(1-b^2+2 b x)}{2 \left(1-b^2\right) x}\in(0,h_b) \end{equation} if $x\ne0$ and $h_{b,x}:=-\frac b{1-b^2}$$h_{b,x}:=-\frac b{1-b^2}\in(0,h_b)$ if $x=0$ (in which latter case necessarily $b=x-y=-y<0$). Thus, the best exponential bound on $P(X>y+b)$ is $\exp\{n\ell_{b,y+b}(h_{b,y+b})\}$. Here is the graph of the exponential rate $\ell_{b,y+b}(h_{b,y+b})$ for $b\in(-1,1)$ and $y\in(0,3)$:

Note also that, according to Theorem 1 on page 495 in [Chernoff, The Annals of Mathematical Statistics, Vol. 23, No. 4 (1952), pp. 493--507], the upper bound $\exp\{n\ell_{b,y+b}(h_{b,y+b})\}$ is optimal in the sense that $$P(X>y+b)=\exp\{n\ell_{b,y+b}(h_{b,y+b})(1+o(1))\}$$ as $n\to\infty$.